Physicians dedicate their lives to patient care, but few realize that even after they’ve stopped practicing, they can still face the risk of medical malpractice claims tied to past services. If you’ve ever wondered what protects a physician after they’ve left a job, moved to another state, or retired from medicine, the answer often lies in tail coverage.

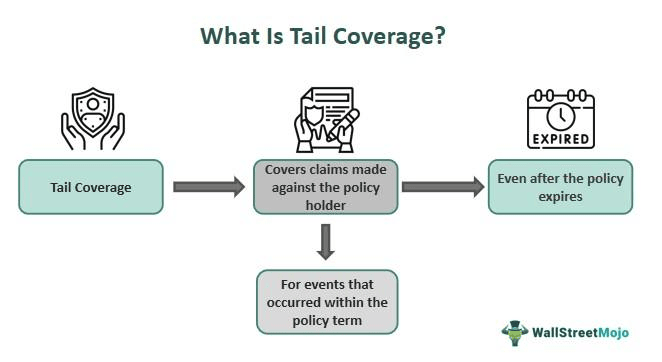

Tail Coverage Insurance for physicians is a vital policy that extends coverage indefinitely beyond the end date of a claims-made malpractice policy.

Without this protection, you could still face lawsuits tied to care you provided years ago—even long after you’ve retired.

Here is an overview of why Tail Coverage Insurance should be included in the risk management strategy for all physicians.

1. Protects Against Future Claims

Unlike occurrence-based policies, which cover incidents based on when they happened, claims-made policies only protect you if the claim is filed while your policy is active. Once that policy ends—either because you leave the job or retire—you’re no longer covered.

That’s where Tail Coverage comes in: they extend your protection, sometimes indefinitely, to cover claims reported after you’ve moved on.

According to the Medical Malpractice Report by the National Practitioner Data Bank (NPDB), approximately 17,000 malpractice payments are made annually in the United States. Many of these claims are filed months or even years after the treatment occurred.

Without tail coverage, you remain financially and legally vulnerable to these delayed lawsuits, even though you’re no longer employed at the practice where the alleged incident occurred.

2. Secures Long-Term Financial Health

A malpractice case can easily amount to six- or seven-figure expenses. Fees for defense alone can be as much as $50,000 to $100,000 per case, even if the doctor is not found to be negligent. Awards or settlements are much higher.

Tail Coverage Insurance ensures you won’t have to pay these costs out-of-pocket. If a claim arises after your active policy ends, you’re still protected. It provides coverage for both legal defense and potential payouts.

Statistic:

As per Medscape’s Malpractice Report 2017, 55% of physicians surveyed had been named in at least one malpractice suit during their careers. These lawsuits often surface long after employment ends.

3. Simplifies Career Transitions

Switching employers already involves stress; ongoing liability from your previous job adds another layer of risk. When switching to a new employer, particularly one with occurrence-based malpractice coverage, it’s absolutely essential to secure a tail policy to cover your record under the old claims-made policy. Failing to do so may leave years of your work unprotected.

Example:

A physician leaves a hospital in 2024 but is sued in 2026 for an act performed in 2023. Without the tail coverage, the physician would have no coverage on that claim.

4. Supports Retirement Planning

Most physicians mistakenly think that malpractice exposure ends when they retire. In reality, years afterward, claims might arise. Tail Coverage Insurance ensures you can fully enjoy retirement without concerns about the economic or legal ramifications of past care.

Example:

The statute of limitations for filing medical malpractice lawsuits varies but often extends to 2-5 years after an injury is discovered, not necessarily after the care occurred. For pediatric cases, this window may remain open until the child reaches adulthood.

5. Strengthens Job Negotiations

Understanding who is responsible for Tail Coverage Insurance can significantly impact an employment offer. A few employers provide it; others ask physicians to purchase it independently. Understanding its worth allows you to negotiate compensation packages more effectively.

Example:

Tail coverage may run 150-250% of the cost of your yearly premium of malpractice insurance. If your yearly premium is $20,000, your tail policy could be $30,000 to $50,000. Getting it clear if your employer pays for this is important during negotiations.

6. Protects Family Finances

A malpractice claim isn’t just risking your finances; it risks your family’s financial security. Without Tail Coverage Insurance, your personal assets may be at risk if you are sued after your employment has ended.

Example:

You are a retired physician, and you are sued and lose your malpractice suit. Without coverage, your retirement assets, home, and estate may be at risk to fund the settlement or judgment issued by the court. Tail insurance protects you from this outcome and gives you peace of mind long-term.

7. Offers Flexibility in Purchasing Options

Different physicians will require different types of coverage. Some will need only five years of coverage, while others will want to continue coverage indefinitely. Tail Coverage Insurance Policies can be tailored for either a set period of coverage or indefinite protection.

You can purchase tail coverage through your existing insurer or obtain a stand-alone policy from a specialty provider.

Example:

An OB/GYN may prefer perpetual tail coverage due to the high-risk nature of their specialty and the potential for lawsuits long after childbirth events. A dermatologist may opt for a shorter coverage window.

8. Helps Maintain Professional Reputation

Your reputation is one of your greatest assets. To defend yourself when a claim is made years after you’ve retired from practice can prove costly and challenging when you’re not covered. Tail policies ensure you have access to top-notch legal teams who will protect your professional reputation as well as your personal reputation.

Even a dismissed case still requires legal defense, which can easily exceed $50,000. Tail coverage gives you the funds to defend yourself and your legacy.

9. Required for Certain Licenses and Contracts

In some states or institutions, Tail Coverage Insurance is mandatory. Hospitals, insurance companies, and licensing boards often require proof of tail coverage before granting privileges, issuing licenses, or approving new policies.

Example:

Some states have mandatory extended reporting periods for medical malpractice claims. Certain hospital groups won’t credential physicians without proof of adequate tail coverage from previous employment.

10. Provides Cost Predictability and Budgeting Clarity

Tail Coverage Insurance Policies typically entail paying a one-time premium in advance, and thus, budgeting is simple. You pay only once and have coverage for the agreed time period or for life. This removes the uncertainty about future payments and allows you to budget your money more confidently.

Example:

Paying a $40,000 lump sum premium upfront could protect you from future seven-figure lawsuits. It’s a smart financial investment in securing your long-term security.

The threat of medical malpractice claims doesn’t end when your career ends. Tail Coverage is a protection that defends the physician against delayed suits regarding past care. It protects your assets, reputation, professional legacy, and the future of your family.

Because statutes of limitations and malpractice statutes vary extensively, collaboration with an experienced insurance consultant ensures awareness of your responsibilities and choices for coverage.

In a career where you’ve given so much to others, Tail Coverage Insurance gives something back: security, peace of mind, and the freedom to enjoy your next chapter without worry.