Leaving a medical practice, retiring, or changing jobs comes with a long to-do list. But for physicians on a “claims-made” insurance policy, one item often carries the biggest price tag: Tail Coverage.

Many doctors assume they are forced to buy this coverage from their current insurance carrier. This misconception often leads to overpaying by thousands of dollars.

The reality? You have options. Stand-alone tail coverage is a flexible, cost-effective alternative that can provide the same “A-rated” protection for a fraction of the price. In this guide, we break down exactly what stand-alone tail coverage is, how much it costs, and why it might be the smartest financial move for your career transition.

What Is Tail Coverage? (And Why Is It Mandatory?)

To understand stand-alone tail coverage, you first need to understand the gap it fills.

Most medical malpractice insurance is written on a “Claims-Made” basis. This means your policy only covers you if it is active both when the incident happened AND when the lawsuit is filed.

The Problem: If you cancel your policy (e.g., you retire or leave a job), you are no longer “active.” If a patient sues you a year later for a surgery you performed three years ago, your old policy will not cover it.

The Solution: Tail coverage—formally known as an Extended Reporting Period (ERP) endorsement—extends your reporting window indefinitely. It ensures you are protected against claims from past procedures, even after your policy has ended.

Deep Dive: Want to master the basics? Read our guide on Tail Policy 101.

The “Hidden” Option: What Is Stand-Alone Tail Coverage?

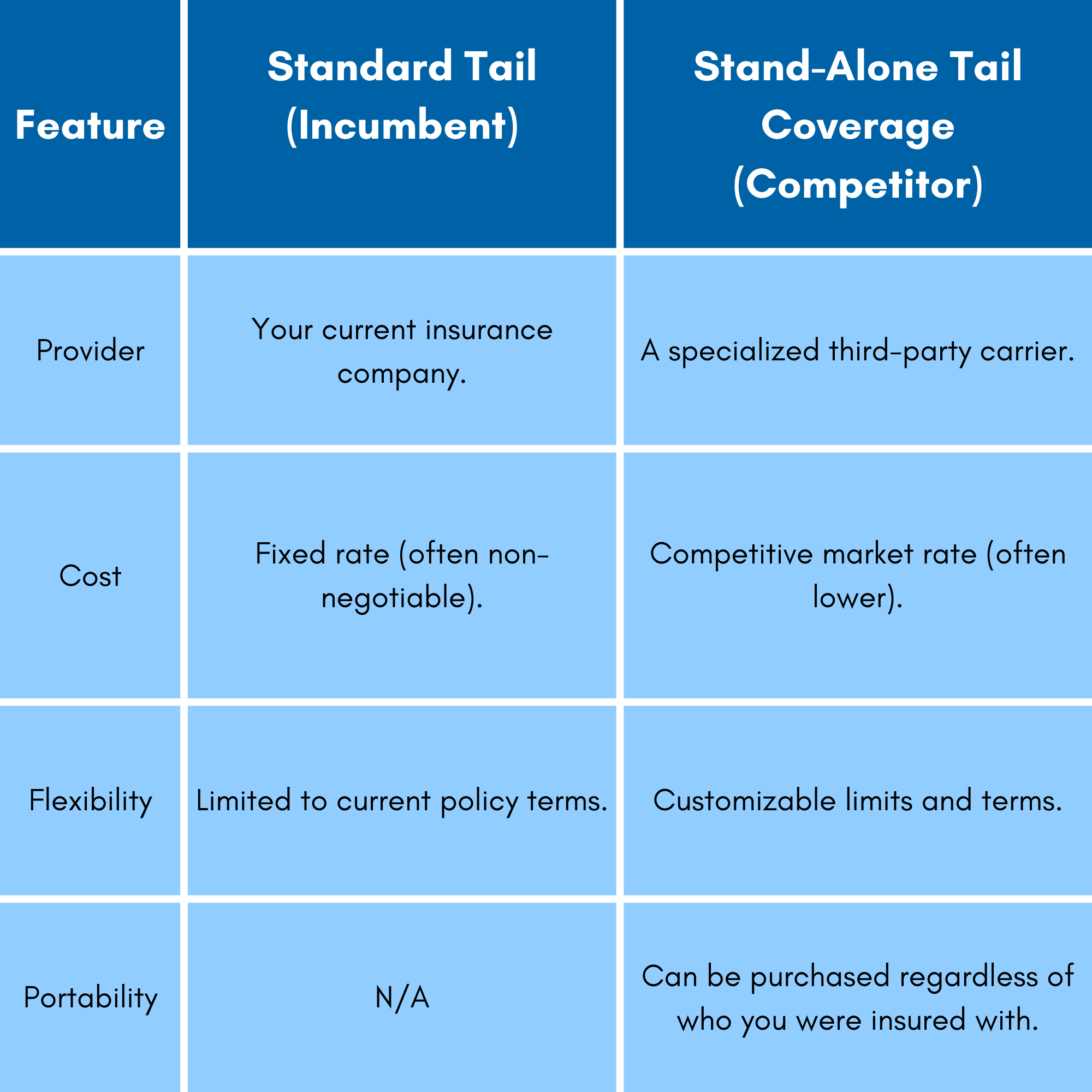

When you leave a job, your current insurer will likely send you a bill for tail coverage. This is “Standard Tail.” It is often expensive because the insurer knows you need it to close the gap.

Stand-Alone Tail Coverage is a separate policy purchased from a different insurance carrier than the one you are leaving.

It works the same way—covering your past acts—but because stand-alone carriers are competing for your business, they often offer significantly better rates and terms.

Key Difference: Standard vs. Stand-Alone

Tail Coverage Cost: How Much Can You Save?

The cost of malpractice tail coverage is typically calculated as a percentage of your maturing annual premium.

- Industry Standard: According to the AANA, physicians can typically expect to pay roughly two times (200%) their annual premium for standard tail coverage.

- The Stand-Alone Advantage: Because stand-alone carriers price risk differently, they can often offer policies for 10% to 35% less than the incumbent carrier’s offer.

Example Scenario:

- Annual Premium: $20,000

- Standard Tail Offer (200%): $40,000

- Stand-Alone Quote (Savings): $28,000 – $34,000

That is a potential savings of $ 6,000 or more just by getting a second quote.

Do I Need Tail Coverage? (3 Common Scenarios)

If you are on an “Occurrence” policy, you generally do not need tail coverage. However, if you have a “Claims-Made” policy, you need stand-alone tail coverage in the following situations:

- Changing Jobs: You are leaving a private practice or hospital that does not provide “nose coverage” (prior acts coverage) at your new job.

- Retirement: You are hanging up your coat. While some carriers offer free travel upon retirement (usually after 5-10 years of loyalty), many physicians do not meet these strict tenure requirements.

Policy Cancellation: Your current insurer is raising rates, or you are switching to a new carrier that won’t cover your past acts.

Benefits of Stand-Alone Tail Coverage

Why should you go through the effort of getting a stand-alone tail coverage quote instead of just paying your current bill?

- Significant Cost Savings: As noted above, the primary benefit is financial. You are purchasing the same product (protection) for a lower price.

- “A” Rated Carriers: You do not have to sacrifice quality. PLI Consultants only works with carriers rated “A-” (Excellent) or better by A.M. Best.

- Refreshed Limits: Some stand-alone policies offer a fresh set of liability limits, rather than sharing the limits of your expiring policy.

- Perpetual Coverage: Most stand-alone policies offer an unlimited reporting period, meaning you are covered for as long as you need it.

How to Get a Stand-Alone Tail Coverage Quote

Don’t let your current carrier pressure you into signing a high-cost renewal. You have the right to shop around.

At PLI Consultants, we specialize in finding physicians the best rates on tail coverage. Because we have access to a nationwide network of specialty carriers, we can quickly compare your current offer against the stand-alone market.

Ready to see your savings?

- Click Here to Request a Free Tail Coverage Quote.

- Use our Tail Coverage Calculator to estimate your costs.