Family Practice physicians serve at the core of primary care, managing everything from chronic conditions and acute illnesses to preventive and mental health services, making broad clinical exposure unavoidable and comprehensive protection essential.

PLI Consultants provides customized, A-rated coverage with flexible policy options, practical risk management support, and potential savings of 10–35%, helping physicians reduce liability exposure while staying focused on patient care.

Family Practice Malpractice Insurance is a specialized professional liability policy designed to protect family physicians against claims of negligence, misdiagnosis, delayed treatment, or medical errors. Given the broad scope of care—ranging from pediatrics to geriatrics—family physicians face diverse clinical exposures.

Without malpractice insurance, a single lawsuit could cost a family physician hundreds of thousands of dollars out of pocket — even if the claim is ultimately dismissed. Given the high volume and broad scope of care that family physicians provide, the liability exposure is both constant and significant.

Family physicians are often surprised to learn that their specialty carries moderate-to-high malpractice risk. The perception that risk is confined to surgical specialists is a common misconception. In reality, the breadth and volume of care provided by family physicians create a wide surface area for potential claims.

General surgery carries one of the highest liability profiles in medicine, and the data confirms it.

83% of general surgeons are named in at least one malpractice lawsuit during their career, tied with plastic surgeons for the most sued specialty in medicine. Claims typically arise from post-operative complications, wound infections, delayed diagnoses, informed consent failures, and, most seriously, wrong-site surgical events.

Florida compounds this risk significantly. The state ranks among the top three in the nation for total malpractice payouts, and its South Florida counties (Dade and Broward) are among the most litigious territories in the country, driving premiums nearly double what a surgeon would pay in the Rest of State territory.

Georgia has historically had high rates, though recent carrier market competition and a $250,000 cap on punitive damages have helped moderate premiums. Tennessee offers the most favorable litigation environment of the three states, with a single statewide territory and significantly lower base rates.

Understanding where you practice, and what your state’s litigation climate looks like, directly determines your premium. PLI Consultants monitors all three markets continuously and knows which carriers are competing aggressively for general surgery business right now.

PLI Consultants operates across all three states and provides access to current market pricing. The figures below reflect established base premiums at standard coverage limits, prior to applying PLI’s 10–35% savings through multi-carrier placement.

Florida classifies physician risk into four to six territories. General surgeons face the widest rate spread of any state PLI serves.

| Territory | General Surgeon Rate (Base) | With PLI Savings (10–35%) |

|---|---|---|

| Dade / Broward | $93,000 | $60,450 – $83,700 |

| West Palm Metro | $71,300 | $46,345 – $64,170 |

| Jacksonville Metro | $63,100 | $41,015 – $56,790 |

| Rest of State | $51,700 | $33,605 – $46,530 |

Rates shown at $250,000/$750,000 limits, Florida’s most common standard. Most hospital systems require $1M/$3M for admitting privileges, see coverage limits section below.

Florida classifies physician risk into four to six territories. Family physicians face meaningful rate variation depending on their geographic location, with South Florida’s litigious environment driving the highest premiums in the state.

| Territory | Family Practice Rate (Base) | With PLI Savings (10–35%) |

|---|---|---|

| Dade / Broward | $22,200 | $19,980 – $14,430 |

| West Palm Metro | $15,700 | $14,130 – $10,205 |

| Jacksonville Metro | $13,100 | $11,790 – $8,515 |

| Rest of State | $11,900 | $10,710 – $7,735 |

Rates shown at $250,000/$750,000 limits, Florida’s most common standard. Unlike surgical specialties, most hospital systems do not require higher limits for family physicians, though many elect $500K/$1.5M or $1M/$3M for broader protection.

Georgia uses two territories. Standard coverage limits in Georgia are $1M per claim / $3M aggregate. Family Practice is one of the more competitively priced specialties in Georgia’s market.

| Territory | Family Practice Rate(Base) | With PLI Savings (10–35%) |

|---|---|---|

| Atlanta Metro | $13,000 | $11,700 – $8,450 |

| Rest of State | $12,400 | $11,160 - $8,060 |

Georgia’s $250,000 cap on punitive damages (Georgia Code § 51-12-5.1) has contributed to market stability. The narrow rate gap between Atlanta Metro and Rest of State reflects the relatively lower litigation intensity for primary care compared to surgical specialties.

Tennessee operates as a single statewide territory for most carriers, making it the most straightforward and cost-effective market for family physicians. With strong tort reform protections and a lower litigation rate, Family Practice premiums in Tennessee are among the most affordable in the PLI Consultants service area.

| Territory | Family Practice Rate(Base) | With PLI Savings (10–35%) |

|---|---|---|

| Statewide (Single Territory) | $8,100 | $7,290 – $5,265 |

Tennessee’s standard limits are $1M/$3M. The single-territory structure and lower litigation rate make Tennessee the most cost-effective of the three states for family physicians — nearly 64% less expensive than the equivalent Dade/Broward rate in Florida.

Georgia uses two territories. Unlike Florida, Georgia’s standard coverage limits are $1M per claim / $3M aggregate, making direct state comparisons important for surgeons licensed in both states.

| Territory | General Surgeon Rate (Base) | With PLI Savings (10–35%) |

|---|---|---|

| Atlanta Metro | $45,100 | $29,315 – $40,590 |

| Large Metro | $40,800 | $29,120 – $40,320 |

| Rest of State | $48,200 | $31,330 – $43,380 |

Georgia’s $250,000 cap on punitive damages (Georgia Code § 51-12-5.1) has helped stabilize the market. New carrier entrants in recent years have increased competition and driven rates down.

| Territory | General Surgeon Rate (Base) | With PLI Savings (10–35%) |

|---|---|---|

| Shelby & Memphis) | $43,200 | $28,080 – $38,880 |

| Nashville & Knoxville | $36,500 | $23,725 – $32,850 |

| Rest of State | $29,800 | $19,370 – $26,820 |

Tennessee’s standard limits are $1M/$3M. The state’s lower litigation rate and single-territory structure make it the most cost-effective of the three states for general surgeons.

PLI Consultants primarily serves neurologists practicing in Florida, Georgia, and Tennessee. Each state has a distinct malpractice environment shaped by state tort laws, litigation history, damages caps, and carrier availability. Here is a high-level comparison:

| Factor | Florida | Georgia | Tennessee |

|---|---|---|---|

| Damages Cap (Non-Economic) | Removed (2023) | $350,000 (standard) | $750,000 (most cases) |

| Litigation Environment | High – frequency claims, large verdicts | Moderate – tort reform in effect | Moderate – balanced environment |

| Mandatory Insurance Requirement | Yes — most settings | No state mandate | No state mandate |

| Typical Neurologist Premium Range | $14,000 – $30,000+ | $10,000 – $22,000 | $9,000 – $20,000 |

| PLI Carrier Access | Multiple A-rated carriers | Multiple A-rated carriers | Multiple A-rated carriers |

State legal minimum

Hospitals Requiring $1M/$3M

Tampa General Hospital

Jackson Memorial Hospital

Baptist Health

Orlando Health

Lakeland Regional Health

Practically universal standard

Hospitals requiring $1M/$3M

Wellstar Health

Piedmont Health

Grady Health System

Tanner Health

Consistent statewide standard

HCA Healthcare (multiple Tennessee campuses)

Vanderbilt University Medical Center

Ballad Health

Baptist Memorial Health Care

The state legal minimum and most common standard is $250,000 per claim / $750,000 aggregate. However, most major Florida hospital systems require $1M/$3M for admitting privileges, including AdventHealth, Tampa General Hospital, Jackson Memorial, Baptist Hospital, Orlando Health, and Lakeland Regional Health. General surgeons who need hospital access effectively require the higher limit.

The standard and practically universal limit is $1M per claim / $3M aggregate. Lower limits are uncommon and rarely accepted by hospital credentialing departments. Georgia hospital systems requiring these limits include Wellstar Health, Piedmont Health, Grady Health System, and Tanner Health.

Standard limits are also $1M per claim / $3M aggregate. The consistent statewide standard simplifies credentialing across Tennessee hospital systems.

Given the broad exposure in family medicine, it’s advisable to carry at least $1M/$3M coverage limits regardless of state minimums, consider occurrence policies for long-term stability, and plan for tail coverage early to avoid significant exit costs. Bundling risk management services can further help reduce premiums while strengthening overall protection.

Not all malpractice policies are created equal. When evaluating coverage options, family physicians should carefully assess the following elements:

Only consider carriers rated A. This rating reflects the carrier’s ability to pay claims. Do not accept a policy from a carrier with a lower rating, regardless of premium savings.

Confirm whether defense costs (attorney fees, expert witnesses) are included within the policy limits or paid in addition to them. “In addition to” (or “outside limits”) coverage is significantly more protective.

If switching carriers, ensure your new policy includes a prior acts endorsement (also called “nosing back”) to cover incidents that occurred before the new policy’s inception date.

Look for policies that require your consent before settling a claim. Some carriers settle without the physician’s agreement, which can affect your National Practitioner Data Bank (NPDB) record.

Verify that the policy covers defense costs for state medical board investigations, not just civil lawsuits. This is critical protection for your license.

If you offer virtual consultations, confirm your policy explicitly covers telemedicine encounters. Many standard policies have exclusions or require a separate endorsement.

If choosing a claims-made policy, understand the tail cost formula. Free tail provisions (for retirement or disability) can save tens of thousands of dollars.

Many top carriers offer premium discounts of 5–10% for completing accredited risk management courses. Ask whether your carrier offers this benefit.

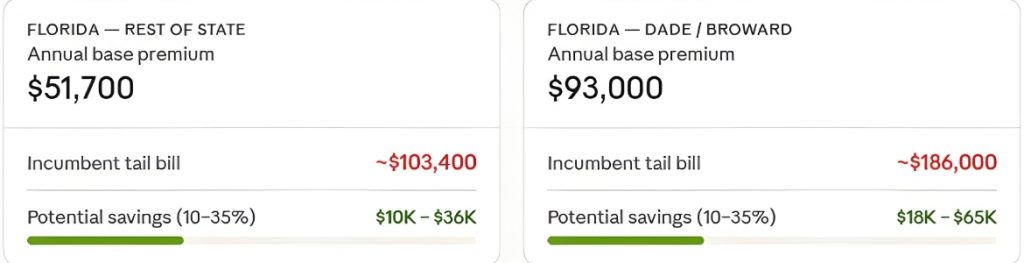

Tail coverage for family physicians is still a meaningful expense — even though base premiums are lower than surgical specialties, the 150% – 200% tail multiplier means a physician paying $11,900–$22,200 annually in Florida is still looking at a five-figure tail bill from their incumbent carrier.

Rest of State Florida ($11,900/yr): ~$23,800 tail bill from incumbent carrier

Dade/Broward ($22,200/yr): ~$44,400 tail bill from incumbent carrier

Atlanta Metro Georgia ($13,000/yr): ~$26,000 tail bill from incumbent carrier

Tennessee Statewide ($8,100/yr): ~$16,200 tail bill from incumbent carrier

PLI Consultants accesses a network of stand-alone tail carriers that compete against your incumbent’s offer. We routinely achieve 10–35% reductions — saving family physicians anywhere from $1,600 to $15,500 on a single tail purchase.

There is no obligation, and the comparison takes one business day.

Family Practice physicians across Florida, Georgia, and Tennessee trust PLI Consultants for one reason: we know this space better than anyone, and we work exclusively in your interest.

Specialty Expertise

One Application, Multiple Quotes

A-Rated Carriers Only

Transparent Pricing

Tail Coverage Savings

Dedicated Advisor

Licensed in Florida, Georgia, and Tennessee

Requirements vary by state. Florida mandates that physicians maintain minimum malpractice coverage or meet financial responsibility requirements. Georgia and Tennessee have similar requirements for licensed practitioners. Additionally, most hospitals, health systems, and credentialing bodies require proof of insurance regardless of state law. PLI Consultants will help you meet all applicable requirements.

A claims-made policy only covers claims that are both incurred and reported while the policy is active. An occurrence policy covers any incident that happens during the policy period, even if the claim is filed years later. Claims-made policies are more common and typically less expensive initially, but they require tail coverage when the policy ends. PLI Consultants will help you evaluate which structure makes more financial sense for your situation.

You need tail coverage if you have a claims-made policy and are leaving your current insurer for any reason — switching carriers, changing employers, retiring, or closing your practice. Without tail coverage, you could be personally liable for claims filed after your policy ends related to care you provided during the coverage period.

Yes. A prior claim does not mean you cannot obtain quality coverage. PLI Consultants works with carriers who specialize in physicians with complex claims histories. We will present your profile in the most favorable light and identify the best available options. Transparency about prior claims is essential — we will guide you through the disclosure process.

It depends on your policy. Some standard policies include telemedicine as part of their base coverage; others require an endorsement or have exclusions for virtual care. PLI Consultants will verify your telehealth exposure is fully covered before your policy is bound.

With PLI Consultants, you complete one application and typically receive multiple quotes within 24–48 business hours. For physicians with straightforward histories, binding can often happen within a few days.

Absolutely. Many carriers offer free tail provisions for retirement after age 55 with sufficient years on the policy. If your carrier does not offer this, PLI Consultants can source standalone tail coverage at a significantly lower cost than your existing carrier’s quoted rate — often 10%–35% less.

We use cookies to improve your experience on our site. By using our site, you consent to cookies.

Manage your cookie preferences below:

Essential cookies enable basic functions and are necessary for the proper function of the website.

These cookies are needed for adding comments on this website.

Google reCAPTCHA helps protect websites from spam and abuse by verifying user interactions through challenges.

Google Tag Manager simplifies the management of marketing tags on your website without code changes.

Statistics cookies collect information anonymously. This information helps us understand how visitors use our website.

Google Analytics is a powerful tool that tracks and analyzes website traffic for informed marketing decisions.

Service URL: policies.google.com (opens in a new window)

Marketing cookies are used to follow visitors to websites. The intention is to show ads that are relevant and engaging to the individual user.

Facebook Pixel is a web analytics service that tracks and reports website traffic.

Service URL: www.facebook.com (opens in a new window)