Healthcare workers often carry malpractice insurance for years without realizing that the most important protection may be needed after a policy ends. This is especially true with claims-made malpractice insurance, where coverage does not automatically follow you once you change jobs, retire, or switch carriers.

This guide explains how tail coverage works, why it is required in a claims-made malpractice policy, how much it typically costs, and how to avoid common and expensive mistakes.

Quick Summary

- Claims-made policies only cover claims filed while the policy is active

- Once a claims-made policy ends, coverage stops unless tail coverage is in place

- Tail coverage allows claims to be reported after the policy ends

- Occurrence policies do not require tail coverage

- Tail coverage cost is often a multiple of your annual premium

- Planning early can significantly reduce tail exposure

What Is Tail Coverage on a Claims-Made Policy?

Tail coverage, also known as an extended reporting period, allows you to report claims after a claims-made malpractice policy has ended, provided the incident occurred while the policy was active. In simple terms:- The care happened in the past

- The claim is filed in the future

- Tail coverage bridges the gap

Does a Claims-Made Policy Need Tail Coverage?

In most cases, yes. A claims-made policy needs tail coverage when:- You leave an employer that provided claims-made coverage

- You retire from clinical practice

- You switch insurance carriers

- Your policy is canceled or non-renewed

How Tail Coverage Works in a Claims-Made Malpractice Policy

To understand how tail coverage works, you must first understand the trigger of a claims-made policy. A claims-made malpractice policy requires:- The incident occurred after the retroactive date

- The claim is filed while the policy is active

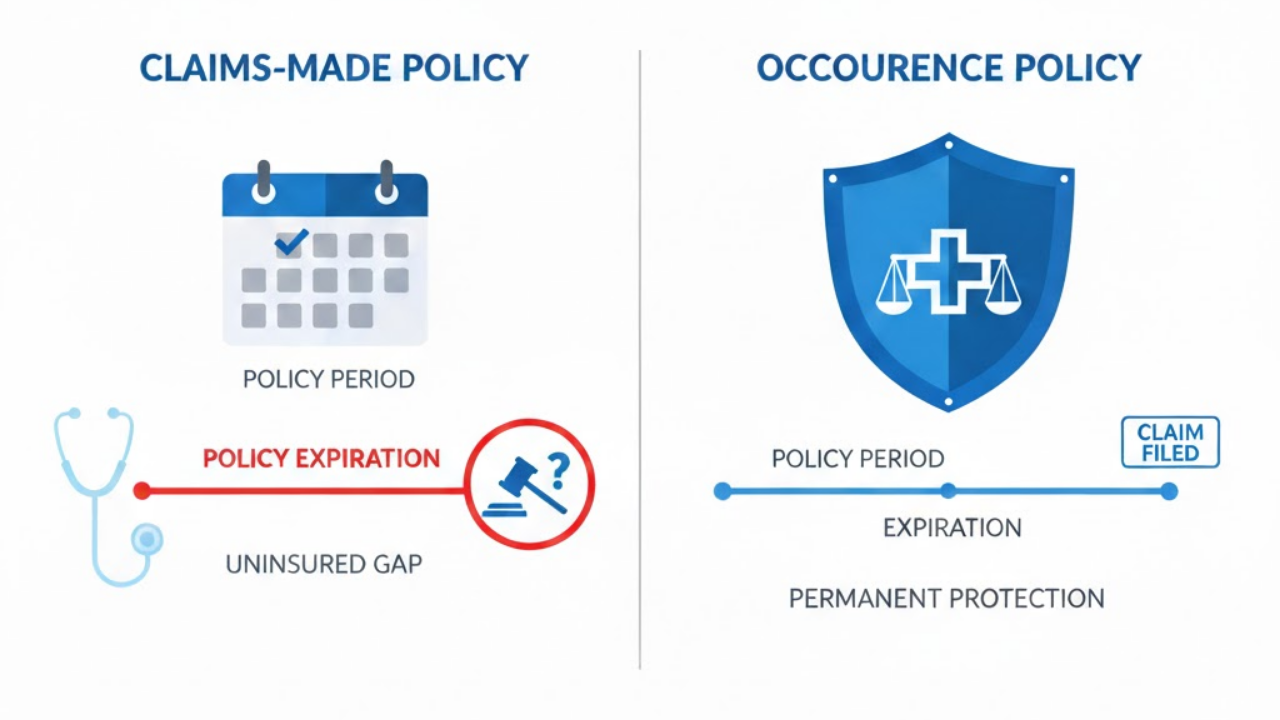

Claims-Made With Tail Coverage vs Occurrence Policy

Claims-Made Policy With Tail Coverage

- Lower premiums in early years

- Tail coverage is required when the policy ends

- The total lifetime cost can be higher if the tail is not planned for

Occurrence Policy

- Higher annual premiums

- No tail coverage required

- Coverage is permanent for each policy year

Buying Tail Coverage After a Claims-Made Policy Ends

Tail coverage is typically purchased:- From the original insurer

- As a one-time, non-cancelable policy

- Within a limited time window after termination

How Much Does Tail Coverage Cost?

Tail coverage cost is one of the most common surprises healthcare workers face. In most cases, tail coverage costs:- 150% to 250% of the final annual premium

- Annual premium: $20,000

- Estimated tail cost: $30,000 to $50,000

Common Tail Coverage Mistakes

Healthcare workers most often run into trouble by:- Assuming the employer pays for tail coverage

- Confusing tail coverage with occurrence coverage

- Waiting until after leaving a job to evaluate options

- Not understanding contract language around insurance obligations

How Tail Coverage Fits Into a Long-Term Insurance Strategy

Tail coverage should never be treated as a last-minute add-on. It should be part of a broader malpractice insurance strategy that considers:- Career stage

- Job mobility

- Retirement plans

- Risk tolerance

- Policy structure