For most healthcare providers, the medical malpractice policy is a significant line item on the annual budget, yet it remains one of the least understood contracts in their portfolio. A common misconception is that “malpractice insurance covers everything related to a lawsuit.”

The reality is more nuanced. Your policy is a specific contract designed to cover professional negligence, but it contains critical exclusions, sub-limits, and clauses that can dramatically affect your financial security and professional reputation.

At PLI Consultants, we believe in empowering physicians with clarity. In this deep-dive analysis, we break down the anatomy of a medical malpractice policy, exposing the “hidden” clauses like the Hammer Clause and explaining the difference between defense costs inside and outside your limits.

1. The Core Components of Coverage (The “Indemnity”)

When a patient files a lawsuit alleging negligence, your policy activates to cover two primary financial buckets: Indemnity and Defense.

A. Economic Damages

If you are found liable, or if a settlement is reached, your policy pays for the patient’s quantifiable financial losses. This includes:

- Medical Expenses: Past and future medical care required as a result of the alleged error.

- Lost Wages: Income the patient lost while recovering, or loss of future earning capacity.

- Rehabilitation Costs: Physical therapy or home modifications.

B. Non-Economic Damages (Pain & Suffering)

This covers subjective harm, such as emotional distress, pain, and loss of enjoyment of life.

- Note for FL, GA, & TN Physicians: Many states have placed statutory caps on non-economic damages to stabilize insurance markets. However, these laws frequently change. Ensuring your policy limits meet or exceed these potential caps is critical.

C. Vicarious Liability

Many physicians are unaware that they can be sued for the actions of their staff.

- What it covers: Liability for errors committed by employees (nurses, technicians, medical assistants) under your supervision.

- The Trap: If you employ another physician or a high-level provider (PA/NP), your individual policy might not automatically cover them. They often require separate limits or a “shared limit” endorsement.

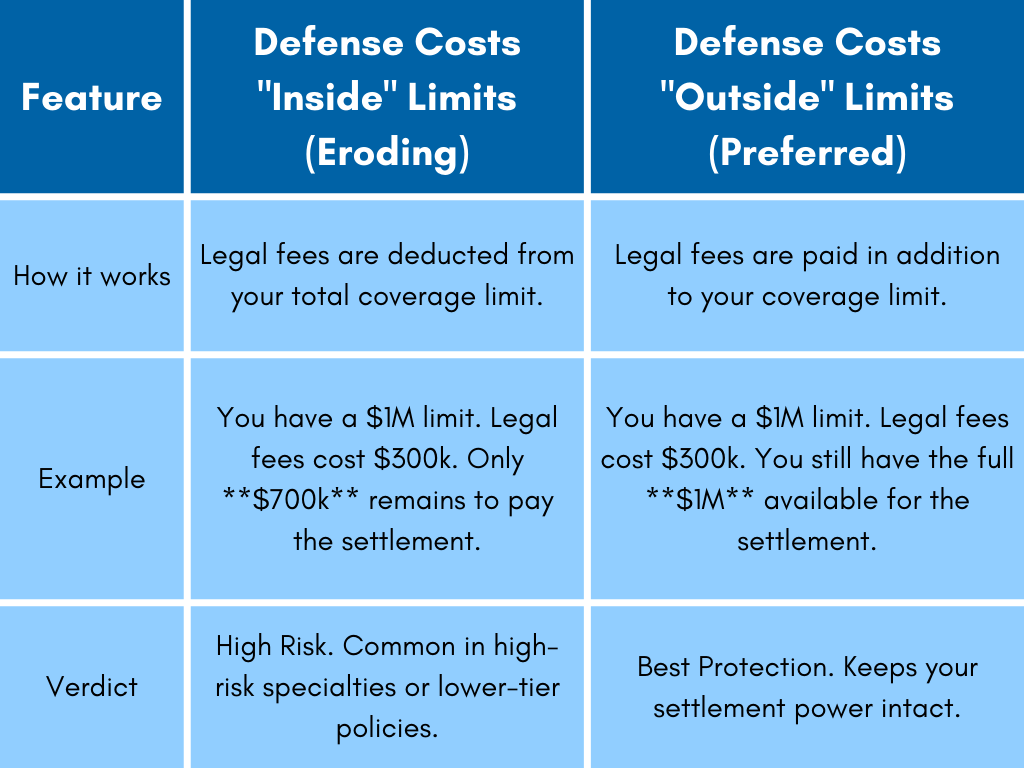

2. Legal Defense Costs: The “Inside vs. Outside” Trap

The most expensive part of a malpractice claim is often the defense, not the settlement. Expert witnesses, depositions, and court fees can easily surpass $100,000.

The critical question you must ask your broker: Are my defense costs “Inside the Limits” or “Outside the Limits”?

PLIC Insight: We always strive to secure “Outside Limits” coverage for our clients whenever available in the marketplace.

3. The “Consent to Settle” & The Hammer Clause

This is the most emotionally charged aspect of a policy. It dictates who gets to decide when to fight and when to fold.

Pure Consent to Settle (The Gold Standard)

Under this hammer clause, the insurance carrier cannot settle a claim without your written permission. If you believe you met the standard of care and want to clear your name in court, you have the power to do so.

The “Hammer Clause” (The Trap)

Some policies contain a provision that limits the insurer’s liability if you refuse to settle.

- Scenario: The insurer wants to settle for $200,000. You refuse because you did nothing wrong.

- The Hammer Drops: If you lose at trial and the jury awards $500,000, the insurer will only pay the $200,000 they originally offered. You are personally liable for the remaining $300,000.

4. Regulatory & License Defense (The “Administrative” Layer)

A malpractice suit often triggers a complaint to the State Board of Medicine. A standard policy’s main limit usually applies only to civil lawsuits for money damages, not administrative hearings.

Check your policy for a “Supplemental Benefit” specifically for Medical Board Defense.

- What it covers: Attorney fees for disciplinary hearings, billing audits (RAC audits), and EMTALA violations.

- Typical Limits: $25,000 to $50,000 (annual aggregate).

5. The “Tail” Issue: Claims-Made Policies

Most malpractice insurance is written on a Claims-Made basis. This means the policy must be active when the incident happens and when the claim is filed.

If you retire, change jobs, or your policy is canceled, you lose coverage for all past acts unless you purchase an Extended Reporting Period (Tail Coverage).

If you want a deeper understanding of how Claims-Made policies differ from Occurrence coverage, including long-term cost implications and when each structure makes sense, review our detailed breakdown on claims-made versus occurrence malpractice insurance.

The PLIC Advantage:

Many doctors assume they must buy Tail Coverage from their current carrier, often at 200%+ of their annual premium. This is false.

At PLI Consultants, we specialize in Stand-Alone Tail Coverage, which often saves physicians 10% to 35% compared to the renewal offer from their incumbent carrier.

6. What Is Strictly EXCLUDED?

Even the best “A-Rated” policies have hard exclusions. You are generally not covered for:

- Criminal Acts: Sexual misconduct or assault (battery).

- Altered Records: Any claim arising where medical records were willfully altered after the fact.

- Business Liability: Slip-and-fall accidents in your waiting room (Requires a General Liability policy).

- Cyber Attacks: Ransomware or HIPAA data breaches (Requires specific Cyber Liability insurance).

Summary: Is Your Practice Truly Protected?

Medical malpractice insurance is not a commodity; it is a complex financial instrument. A policy with “Cheap Premiums” often hides “Inside Limits” or a restrictive “Hammer Clause.”

Your Next Step:

Don’t wait for a claim to discover the holes in your coverage. Let our team review your current policy or provide a competitive quote for your new practice.

- Looking for Tail Coverage? Calculate your potential savings here.

- Need a Policy Review? Contact PLI Consultants today.

PLI Consultants – Specialized advisors for Florida, Georgia, and Tennessee physicians.

FAQ

1. What does medical malpractice insurance actually cover?

Medical malpractice insurance covers the financial and legal consequences of claims alleging negligence or medical errors. This typically includes attorney fees, court costs, settlements, and judgments, ensuring physicians are protected from costly lawsuits.

2. Does malpractice insurance cover legal defense costs?

Yes, malpractice insurance covers legal defense costs, even if the claim is unfounded. The insurer appoints legal counsel and pays for attorney fees, expert witnesses, and court-related expenses, allowing physicians to focus on patient care.

3. Are settlements and court judgments included in coverage?

Malpractice insurance covers settlements and court-awarded damages up to the policy limits. This protection prevents physicians from paying out-of-pocket for large claims resulting from alleged medical negligence.

4. Does medical malpractice insurance include regulatory or licensing support?

Many policies include coverage for medical board investigations or regulatory actions, helping physicians defend their licenses and professional reputation during disciplinary proceedings.

5. What is not covered under malpractice insurance?

Medical malpractice insurance does not cover intentional misconduct, criminal acts, or fraudulent behavior. It is designed strictly for unintentional errors or negligence that occur during the course of providing medical care.