Neurologists face unique malpractice risks due to the complexity of diagnosing and treating neurological conditions. From misdiagnosed strokes to medication errors in epilepsy management, the stakes are high.

PLI Consultants specializes in securing comprehensive, cost-effective malpractice insurance tailored specifically for neurologists practicing across the United States. Compare quotes and save up to 35% on your malpractice insurance today.

Neurologist malpractice insurance provides financial and legal protection when patients claim negligence or errors in diagnosis, treatment, or patient care. This coverage is essential for neurologists, given the intricate nature of neurological diagnostics and the severe consequences of misdiagnosis.

Without this protection, a single malpractice claim could expose a neurologist to hundreds of thousands of dollars in out-of-pocket legal expenses — even if the claim is ultimately dismissed.

Neurology consistently ranks among the higher-risk medical specialties for malpractice claims. Approximately 62% of neurologists will face at least one malpractice claim during their career. Understanding these risk factors is essential for proper coverage planning.

Diagnostic Challenges

Similar symptoms increase misdiagnosis risk.

Time-Critical Treatment

Treatment delays raise liability exposure.

Severe Patient Outcomes

Errors often cause disability or death.

Medication Complications

Dosing and monitoring mistakes trigger claims.

Informed Consent Risks

Poor consent documentation creates legal risk.

General surgery carries one of the highest liability profiles in medicine, and the data confirms it.

83% of general surgeons are named in at least one malpractice lawsuit during their career, tied with plastic surgeons for the most sued specialty in medicine. Claims typically arise from post-operative complications, wound infections, delayed diagnoses, informed consent failures, and, most seriously, wrong-site surgical events.

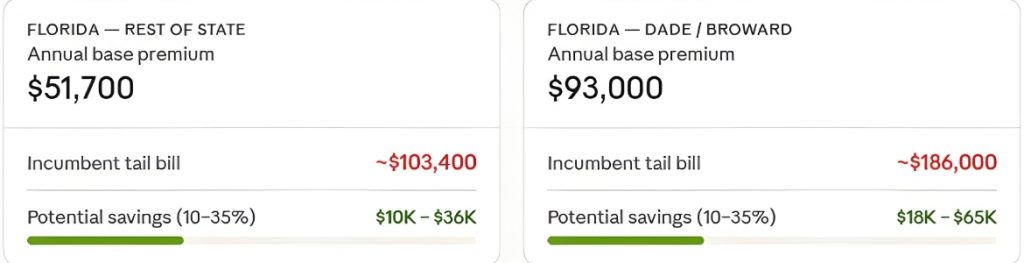

Florida compounds this risk significantly. The state ranks among the top three in the nation for total malpractice payouts, and its South Florida counties (Dade and Broward) are among the most litigious territories in the country, driving premiums nearly double what a surgeon would pay in the Rest of State territory.

Georgia has historically had high rates, though recent carrier market competition and a $250,000 cap on punitive damages have helped moderate premiums. Tennessee offers the most favorable litigation environment of the three states, with a single statewide territory and significantly lower base rates.

Understanding where you practice, and what your state’s litigation climate looks like, directly determines your premium. PLI Consultants monitors all three markets continuously and knows which carriers are competing aggressively for general surgery business right now.

Neurologist malpractice insurance premiums vary significantly based on location, claims history, coverage limits, and practice type. Understanding these cost factors helps you budget appropriately and identify savings opportunities.

Florida classifies physician risk into four to six territories. General surgeons face the widest rate spread of any state PLI serves.

| Territory | General Surgeon Rate (Base) | With PLI Savings (10–35%) |

|---|---|---|

| Dade / Broward | $93,000 | $60,450 – $83,700 |

| West Palm Metro | $71,300 | $46,345 – $64,170 |

| Jacksonville Metro | $63,100 | $41,015 – $56,790 |

| Rest of State | $51,700 | $33,605 – $46,530 |

Rates shown at $250,000/$750,000 limits, Florida’s most common standard. Most hospital systems require $1M/$3M for admitting privileges, see coverage limits section below.

Florida classifies physician risk into four to six territories. Neurologists managing a primarily diagnostic and outpatient practice face meaningful rate variation depending on geographic location and whether procedural work (EMG, nerve conduction studies, lumbar punctures) is included in their scope.

| Territory | Neurologists Rate (Base) | With PLI Savings (10–35%) |

|---|---|---|

| Dade / Broward | $40,100 | $36,090 – $26,065 |

| West Palm Metro | $25,400 | $22,860 – $16,510 |

| Jacksonville Metro | $22,500 | $20,250 – $14,625 |

| Rest of State | $19,300 | $17,370 – $12,545 |

Rates shown at $250,000/$750,000 limits, Florida’s most common standard. Most hospital systems require $1M/$3M for admitting and procedural privileges — see the coverage limits section above. Neurologists performing interventional procedures or hospital-based work should expect rates 15–25% above the base figures shown.

Georgia uses two to three territories. Standard coverage limits in Georgia are $1M per claim / $3M aggregate, making direct comparisons with Florida important for neurologists licensed in both states.

| Territory | Neurologists Rate (Base) | With PLI Savings (10–35%) |

|---|---|---|

| Atlanta Metro | $22,400 | $22,160 – $14,560 |

| Rest of State | $18,900 | $17,010 - $12,285 |

Georgia’s $250,000 punitive damages cap (GA Code § 51-12-5.1) helps stabilize malpractice premiums for neurologists. Physicians with clean claims histories—especially outside the Atlanta metro—often secure lower rates, with strong insurer competition further reducing costs for outpatient neurology practices.

Tennessee offers one of the most cost-effective malpractice environments for neurologists. With a single statewide territory structure, a lower litigation rate, and a $750,000 cap on non-economic damages in most cases, premiums remain more consistent and affordable across the state.

| Territory | Neurologists Rate (Base) | With PLI Savings (10–35%) |

|---|---|---|

| Statewide (Single Territory) | $12,000 | $10,800 – $7,800 |

Tennessee’s standard limits are $1M/$3M. The state’s lower litigation rate, statutory damages cap, and consistent territory structure make it the most cost-effective of the three states for neurologists — particularly those in outpatient or diagnostic-focused practices.

Georgia uses two territories. Unlike Florida, Georgia’s standard coverage limits are $1M per claim / $3M aggregate, making direct state comparisons important for surgeons licensed in both states.

| Territory | General Surgeon Rate (Base) | With PLI Savings (10–35%) |

|---|---|---|

| Atlanta Metro | $45,100 | $29,315 – $40,590 |

| Large Metro | $40,800 | $29,120 – $40,320 |

| Rest of State | $48,200 | $31,330 – $43,380 |

Georgia’s $250,000 cap on punitive damages (Georgia Code § 51-12-5.1) has helped stabilize the market. New carrier entrants in recent years have increased competition and driven rates down.

| Territory | General Surgeon Rate (Base) | With PLI Savings (10–35%) |

|---|---|---|

| Shelby & Memphis) | $43,200 | $28,080 – $38,880 |

| Nashville & Knoxville | $36,500 | $23,725 – $32,850 |

| Rest of State | $29,800 | $19,370 – $26,820 |

Tennessee’s standard limits are $1M/$3M. The state’s lower litigation rate and single-territory structure make it the most cost-effective of the three states for general surgeons.

PLI Consultants primarily serves neurologists practicing in Florida, Georgia, and Tennessee. Each state has a distinct malpractice environment shaped by state tort laws, litigation history, damages caps, and carrier availability. Here is a high-level comparison:

| Factor | Florida | Georgia | Tennessee |

|---|---|---|---|

| Damages Cap (Non-Economic) | Removed (2023) | $350,000 (standard) | $750,000 (most cases) |

| Litigation Environment | High – frequency claims, large verdicts | Moderate – tort reform in effect | Moderate – balanced environment |

| Mandatory Insurance Requirement | Yes — most settings | No state mandate | No state mandate |

| Typical Neurologist Premium Range | $14,000 – $30,000+ | $10,000 – $22,000 | $9,000 – $20,000 |

| PLI Carrier Access | Multiple A-rated carriers | Multiple A-rated carriers | Multiple A-rated carriers |

Rates shown at $250,000/$750,000 limits, Florida’s most common standard. Most hospital systems require $1M/$3M for admitting and procedural privileges — see the coverage limits section above. Neurologists performing interventional procedures or hospital-based work should expect rates 15–25% above the base figures shown.

State legal minimum

Hospitals requiring $2M/$4M

Tampa General Hospital

Jackson Memorial

Baptist Health

Orlando Health

Lakeland Regional Health

Practically universal standard

Hospitals requiring $1M/$3M

Wellstar Health

Piedmont Health

Grady Health System

Tanner Health

Consistent statewide standard

The state legal minimum and most common standard is $250,000 per claim / $750,000 aggregate. However, most major Florida hospital systems require $1M/$3M for admitting privileges, including AdventHealth, Tampa General Hospital, Jackson Memorial, Baptist Hospital, Orlando Health, and Lakeland Regional Health. General surgeons who need hospital access effectively require the higher limit.

The standard and practically universal limit is $1M per claim / $3M aggregate. Lower limits are uncommon and rarely accepted by hospital credentialing departments. Georgia hospital systems requiring these limits include Wellstar Health, Piedmont Health, Grady Health System, and Tanner Health.

Standard limits are also $1M per claim / $3M aggregate. The consistent statewide standard simplifies credentialing across Tennessee hospital systems.

Given the high diagnostic complexity, time-sensitive decision-making, and potential for catastrophic patient outcomes in neurology, we recommend $1M/$3M coverage limits regardless of state minimum requirements. Diagnostic errors and delayed treatment are among the leading causes of claims, often resulting in severe, lifelong disability and high indemnity payouts.

Not all malpractice policies are created equal. When evaluating coverage options, neurologists should look beyond the premium and examine the full policy for the following critical features:

Only consider coverage from AM Best A-rated or better carriers. Financial strength determines the carrier's ability to pay claims — especially the large, multi-year cases that neurological malpractice can produce.

Match your limits to your actual risk exposure. For most neurologists in active clinical practice, $1,000,000 per occurrence / $3,000,000 aggregate is a widely accepted baseline. Higher-risk settings may warrant higher limits.

Some policies pay defense costs inside the policy limits, which reduces the amount available for indemnity payments. Policies that pay defense costs outside (in addition to) the limits offer superior protection and are preferable for neurologists facing complex, lengthy claims.

A strong policy should give you meaningful input on settlement decisions. A 'hammer clause' policy that penalizes you for refusing a settlement can be detrimental to your reputation. Look for a true consent-to-settle provision or negotiate the terms carefully.

Understand the cost of tail coverage before you sign your policy. Some carriers offer free tail upon death, disability, or retirement. Others build in tail premium guarantees. PLI Consultants reviews these provisions for every client.

If you practice or provide telemedicine consultations across state lines, confirm that your policy provides coverage for all jurisdictions where you practice.

If moving from one carrier to another, the retroactive date on a Claims-Made policy is critical. Ensure your new policy's retroactive date matches or precedes your original policy inception date, or that you have explicit nose coverage arranged.

Tail coverage is a significant financial obligation for neurologists because it is directly tied to your expiring claims-made premium. While neurology is considered a moderate-risk specialty, the long-tail nature of diagnostic claims (e.g., missed stroke, delayed diagnosis) increases exposure duration — which directly impacts tail pricing.

Neurologists typically carry lower annual premiums than surgical specialties, but the tail multiplier remains the same, making the exit cost substantial relative to income.

Average Neurologist Premium ($10,000–$30,000/yr): ~$15,000 to $60,000 tail bill from incumbent carrier

Higher-Cost Markets (e.g., $40,000/yr in major metros): ~$60,000 to $100,000 tail obligation

PLI Consultants accesses a nationwide network of stand-alone tail carriers that compete directly with incumbent insurers. By leveraging this competitive marketplace, we consistently achieve 10–35% savings, helping neurologists reduce tail costs by approximately $5,000 to $30,000+ on a single purchase.

There is no obligation, and the comparison takes one business day.

PLI Consultants is exclusively focused on serving healthcare professionals. We are not a generalist insurance agency offering malpractice as a sideline—this is our sole area of specialization, and general surgery represents one of our highest-volume specialties across all three states.

Specialty Expertise

Market Access

One-Application Efficiency

Tail Coverage Savings

Personalized Guidance

No Pressure, No Sales Gimmicks

Trusted by Physicians Across FL, GA & TN

While many hospitals provide coverage, you should still consider personal coverage because hospital policies may not cover moonlighting or telemedicine outside the facility, you may need tail coverage if you leave employment, and hospital coverage may have shared limits that could be exhausted by other providers’ claims.

Claims-made policies cover incidents that occurred AND were reported while the policy was active and require tail coverage when terminated. Occurrence policies cover any incident that occurred during the policy period, regardless of when it’s reported, with no tail coverage needed. Claims-made policies have lower initial premiums but require expensive tail coverage. Occurrence policies cost more upfront but eliminate tail expenses long-term.

Part-time premiums are typically calculated as a percentage of full-time rates based on hours worked: 20 hours/week or less = 50-60% of full-time premium; 21-30 hours/week = 70-80%; 31+ hours/week = 90-100%. Specific calculations vary by carrier.

Many policies include coverage for state medical board defense, often called ‘disciplinary proceeding coverage’ or ‘medical board defense coverage.’ Review your policy or ask your PLI consultant to confirm this coverage is included.

Most modern neurologist malpractice policies include telemedicine coverage, but you must verify coverage applies to all states where you provide telemedicine, technology failure scenarios are covered, and there are no exclusions for remote diagnosis or treatment. As teleneurology expands, this coverage is increasingly important.

We use cookies to improve your experience on our site. By using our site, you consent to cookies.

Manage your cookie preferences below:

Essential cookies enable basic functions and are necessary for the proper function of the website.

These cookies are needed for adding comments on this website.

Google reCAPTCHA helps protect websites from spam and abuse by verifying user interactions through challenges.

Google Tag Manager simplifies the management of marketing tags on your website without code changes.

Statistics cookies collect information anonymously. This information helps us understand how visitors use our website.

Google Analytics is a powerful tool that tracks and analyzes website traffic for informed marketing decisions.

Service URL: policies.google.com (opens in a new window)

Marketing cookies are used to follow visitors to websites. The intention is to show ads that are relevant and engaging to the individual user.

Facebook Pixel is a web analytics service that tracks and reports website traffic.

Service URL: www.facebook.com (opens in a new window)