Obstetrics and gynecology represents one of the highest-risk medical specialties, with prolonged tail exposure and claim severity that can reshape a career. Premiums for OB/GYNs vary dramatically across Florida, Georgia, and Tennessee due to differing litigation climates, state regulations, and regional claim frequencies.

PLI Consultants simplifies the complex process of securing optimal coverage by comparing top A-rated carriers through one streamlined application, helping you find comprehensive protection at the most competitive rates. Compare quotes and save up to 35% on your malpractice insurance today.

OB/GYN malpractice insurance provides essential protection against the unique liability exposures inherent to obstetric and gynecological practice. Given that OB/GYNs have the longest statute of limitations in medicine—often extending 20+ years for birth-related injuries—comprehensive coverage is non-negotiable.

Annual premiums for OB/GYNs range from approximately $48,000 in Tennessee to $127,000+ in high-risk Florida territories. PLI Consultants specializes in helping OB/GYNs across Florida, Georgia, and Tennessee access competitive quotes from A-rated carriers through a single application, typically achieving 10–35% savings over standard market rates.

Obstetrics and gynecology consistently rank as one of the most litigated medical specialties in the United States, and the numbers confirm why insurers classify OB/GYNs as high-risk.

85% of OB/GYNs will face at least one malpractice lawsuit during their career higher than nearly every other specialty. The combination of obstetric unpredictability, surgical complexity, and extended liability periods creates a perfect storm for claims.

Primary claim triggers include:

General surgery carries one of the highest liability profiles in medicine, and the data confirms it.

83% of general surgeons are named in at least one malpractice lawsuit during their career, tied with plastic surgeons for the most sued specialty in medicine. Claims typically arise from post-operative complications, wound infections, delayed diagnoses, informed consent failures, and, most seriously, wrong-site surgical events.

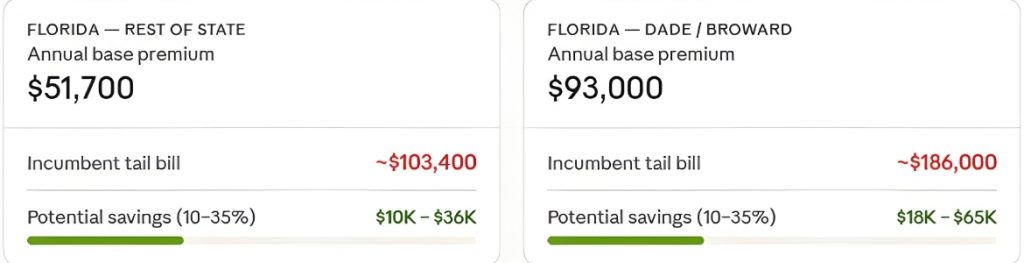

Florida compounds this risk significantly. The state ranks among the top three in the nation for total malpractice payouts, and its South Florida counties (Dade and Broward) are among the most litigious territories in the country, driving premiums nearly double what a surgeon would pay in the Rest of State territory.

Georgia has historically had high rates, though recent carrier market competition and a $250,000 cap on punitive damages have helped moderate premiums. Tennessee offers the most favorable litigation environment of the three states, with a single statewide territory and significantly lower base rates.

Understanding where you practice, and what your state’s litigation climate looks like, directly determines your premium. PLI Consultants monitors all three markets continuously and knows which carriers are competing aggressively for general surgery business right now.

PLI Consultants operates directly in Florida, Georgia, and Tennessee with real-time access to carrier pricing. The rates below represent mature physician base rates at standard coverage limits, before PLI’s typical 10–35% multi-carrier savings are applied.

Florida classifies physician risk into four to six territories. General surgeons face the widest rate spread of any state PLI serves.

| Territory | General Surgeon Rate (Base) | With PLI Savings (10–35%) |

|---|---|---|

| Dade / Broward | $93,000 | $60,450 – $83,700 |

| West Palm Metro | $71,300 | $46,345 – $64,170 |

| Jacksonville Metro | $63,100 | $41,015 – $56,790 |

| Rest of State | $51,700 | $33,605 – $46,530 |

Rates shown at $250,000/$750,000 limits, Florida’s most common standard. Most hospital systems require $1M/$3M for admitting privileges, see coverage limits section below.

Florida classifies physician risk into multiple territories, and OB/GYNs experience the widest premium variance of any specialty PLI serves.

| Territory | OB/GYN Rate (Base) | With PLI Savings (10–35%) |

|---|---|---|

| Dade / Broward | $95,200 | $85,680 – $61,880 |

| West Palm Metro | $75,200 | $67,680 – $48,880 |

| Jacksonville Metro | $64,300 | $57,870 – $41,795 |

| Rest of State | $55,000 | $49,500 – $35,750 |

Rates shown at $250,000/$750,000 limits, Florida’s most common standard. Most hospital systems require $1M/$3M for admitting privileges—see coverage limits section below.

Georgia uses a territorial system with more moderate rate variation. Unlike Florida, Georgia’s standard coverage limits are $1M per claim / $3M aggregate, making direct comparisons essential for physicians licensed in multiple states.

| Territory | OB/GYN Rate (Base) | With PLI Savings (10–35%) |

|---|---|---|

| Atlanta Metro | $74,900 | $67,410 – $48,685 |

| Large Metro | $70,300 | $63,270 – $45,695 |

| Rest of State | $76,600 | $68,940 – $49,790 |

Georgia’s $250,000 cap on punitive damages has helped moderate the malpractice climate. Recent carrier entrants have increased market competition, driving rates down over the past several years.

Tennessee offers one of the most cost-effective malpractice environments for OB/GYNs. The state operates under a single statewide territory with lower litigation frequency and more predictable claim patterns.

| Territory | OB/GYN Rate (Base) | With PLI Savings (10–35%) |

|---|---|---|

| Shelby & Memphis) | $43,500 | $39,150 – $28,275 |

| Nashville & Knoxville | $55,000 | $49,500 – $35,750 |

| Rest of State | $43,900 | $39,510 – $28,535 |

Tennessee’s standard limits are $1M/$3M. The state’s single-territory structure and lower litigation rate make it the most affordable of the three states for practicing OB/GYNs.

Georgia uses two territories. Unlike Florida, Georgia’s standard coverage limits are $1M per claim / $3M aggregate, making direct state comparisons important for surgeons licensed in both states.

| Territory | General Surgeon Rate (Base) | With PLI Savings (10–35%) |

|---|---|---|

| Atlanta Metro | $45,100 | $29,315 – $40,590 |

| Large Metro | $40,800 | $29,120 – $40,320 |

| Rest of State | $48,200 | $31,330 – $43,380 |

Georgia’s $250,000 cap on punitive damages (Georgia Code § 51-12-5.1) has helped stabilize the market. New carrier entrants in recent years have increased competition and driven rates down.

| Territory | General Surgeon Rate (Base) | With PLI Savings (10–35%) |

|---|---|---|

| Shelby & Memphis) | $43,200 | $28,080 – $38,880 |

| Nashville & Knoxville | $36,500 | $23,725 – $32,850 |

| Rest of State | $29,800 | $19,370 – $26,820 |

Tennessee’s standard limits are $1M/$3M. The state’s lower litigation rate and single-territory structure make it the most cost-effective of the three states for general surgeons.

“OB/GYNs in Miami-Dade County can pay several times more for malpractice insurance than physicians in lower-risk rural states like Tennessee, reflecting the region’s higher litigation frequency and claim severity. For OB/GYNs licensed in multiple states or considering practice relocation, this cost differential has profound long-term financial implications.”

Tennessee operates as a single statewide territory; your premium does not vary whether you practice in Memphis, Nashville, or Chattanooga. This simplifies the quoting process and makes Tennessee one of the most transparent markets PLI serves.

Coverage limits are not uniform across Florida, Georgia, and Tennessee, and selecting inadequate limits can jeopardize hospital privileges and expose you to personal liability.

State legal minimum

Hospitals requiring $1M/$3M

Tampa General Hospital

Jackson Memorial

Baptist Health South Florida

Orlando Health

Lakeland Regional Health

Practically universal standard

Hospitals requiring $1M/$3M

Wellstar Health System

Piedmont Healthcare

Grady Health System

Northside Hospital

Emory Healthcare

Consistent statewide standard

The state legal minimum and most common standard is $250,000 per claim / $750,000 aggregate. However, most major Florida hospital systems require $1M/$3M for admitting privileges, including AdventHealth, Tampa General Hospital, Jackson Memorial, Baptist Hospital, Orlando Health, and Lakeland Regional Health. General surgeons who need hospital access effectively require the higher limit.

The standard and practically universal limit is $1M per claim / $3M aggregate. Lower limits are uncommon and rarely accepted by hospital credentialing departments. Georgia hospital systems requiring these limits include Wellstar Health, Piedmont Health, Grady Health System, and Tanner Health.

Standard limits are also $1M per claim / $3M aggregate. The consistent statewide standard simplifies credentialing across Tennessee hospital systems.

Given the high claim severity typical of obstetric cases—particularly birth injury claims that can exceed $10 million in settlements—and the extended statute of limitations unique to OB/GYN practice, we strongly recommend $1M/$3M limits regardless of state minimum requirements.

The premium difference between $250K/$750K and $1M/$3M is often smaller than physicians expect, while the protection gap is enormous. A single severe birth injury claim can easily exhaust lower limits, exposing you to personal asset liability.

Additionally, many insurance carriers apply restrictive underwriting to OB/GYNs who carry substandard limits, viewing it as a risk management red flag.

Not all malpractice policies are created equal, especially for high-risk obstetric specialties. These are the critical features PLI specifically evaluates when comparing carrier options for OB/GYNs:

The insurer cannot force you to settle a claim without your explicit approval. Avoid policies with "hammer clauses" that penalize you financially for refusing settlement. Forced settlements trigger National Practitioner Data Bank (NPDB) reporting, which can impact future credentialing, insurance applications, and professional reputation.

Policies should allow early reporting of concerning incidents—abnormal fetal heart tracings, unexpected surgical complications, or patient complaints—before formal lawsuits are filed. Early incident reporting provides time to develop defense strategies and document events while memories are fresh.

Choose policies where legal defense costs do not erode your coverage limits. OB/GYN cases often require $300K–$500K+ in defense expenses for expert witnesses, depositions, and trial preparation. If defense costs come out of your $1M limit, a resolved claim could leave you with only $500K–$700K in remaining protection.

Every claims-made policy creates tail liability when coverage ends. For OB/GYNs paying $71K–$127K annually in Florida, a standard 200–250% tail multiplier from your incumbent carrier translates to a $142K–$317K lump-sum tail bill at career transition.

Standard tail coverage provides unlimited duration for most specialties, but verify this explicitly in your policy. Some carriers cap tail duration at 5–10 years, which is inadequate for OB/GYN practice given birth injury statutes of limitation that can extend 20+ years.

Florida, Georgia, and Tennessee all maintain active state medical boards. License defense coverage pays for separate legal representation during board investigations, complaints, and disciplinary proceedings—distinct from clinical malpractice claim defense. This protection preserves your ability to practice while claims are being resolved.

Tail coverage is disproportionately expensive for OB/GYNs because tail pricing is calculated as a percentage of your expiring annual premium. The higher your base premium, the larger the tail bill.

An OB/GYN paying $71,400 in Rest of State Florida faces a ~$142,800–$178,500 tail bill from their incumbent carrier

An OB/GYN paying $127,000 in Dade/Broward County faces a ~$254,000–$317,500 tail bill

Additionally, OB/GYNs face extended tail exposure. Birth injury claims can be filed up to 20+ years after delivery in some jurisdictions, meaning tail coverage must provide extended or unlimited reporting duration—not the standard 3–5 year caps some specialties accept.

PLI Consultants accesses a network of stand-alone tail carriers that compete directly against your incumbent carrier’s renewal offer. We routinely achieve 10–35% reductions on tail premiums, saving OB/GYNs anywhere from $14,000 to $110,000+ on a single tail purchase.

There is no obligation, and the tail comparison process takes one business day. The savings can be substantial.

PLI Consultants works exclusively with healthcare professionals. We are not a general insurance agency that happens to offer malpractice coverage—this is the only market we operate in, and OB/GYN is one of our highest-volume specialties across all three states.

One application. Every major carrier.

Licensed in all three states.

OB/GYNs save 10–35%.

Tail coverage expertise.

Obstetric-specific underwriting knowledge.

OB/GYNs in Florida pay between $71,400 (Rest of State) and $127,000 (Dade/Broward County) annually at standard $250K/$750K limits. However, most hospital systems require $1M/$3M limits, which increase premiums accordingly. PLI Consultants typically achieves 10–35% reductions from these base market rates by comparing competing A-rated carriers through a single application.

In Georgia, OB/GYNs pay $58,300 (Large Metro) to $66,100 (Rest of State) at standard $1M/$3M limits. Georgia’s standard limits are higher than Florida’s minimum, which is why direct state comparisons require adjusting for limit differences. PLI achieves 10–35% savings in the Georgia market through multi-carrier competition.

Tennessee OB/GYNs pay approximately $43,900–$58,700 statewide at $1M/$3M limits, representing the lowest base rates of the three states PLI serves. Tennessee operates as a single territory, so rates don’t vary by city. PLI can typically reduce these rates further by 10–35% through carrier comparison.

In Georgia and Tennessee, $1M/$3M is the standard and practically universal requirement. In Florida, the legal minimum is $250K/$750K, but most hospital systems—including AdventHealth, Tampa General, Jackson Memorial, and Baptist Health—require $1M/$3M for admitting and surgical privileges. OB/GYNs who need hospital access in Florida effectively require the higher limit. Given the high severity of birth injury claims, PLI strongly recommends $1M/$3M limits regardless of state minimums.

If you are on a claims-made policy (the most common type), your coverage ends when the policy terminates. Any claim filed after your departure for deliveries or procedures you performed while covered will be unprotected unless you purchase tail coverage (Extended Reporting Period). This is especially critical for OB/GYNs because birth injury claims can be filed 20+ years after delivery. PLI specializes in stand-alone tail policies for OB/GYNs and typically saves 10–35% compared to purchasing tail from your incumbent carrier.

Tail coverage is priced as a multiple of your annual premium—typically 200–250% for OB/GYNs. Since OB/GYN base premiums are already among the highest in medicine ($71K–$127K+ annually in Florida), the resulting tail bill is proportionally massive ($142K–$317K+). Additionally, OB/GYN tail must provide extended or unlimited reporting duration due to the 20+ year statute of limitations for birth injuries, which increases cost further. PLI Consultants accesses competitive stand-alone tail markets that reduce these costs by 10–35%.

We use cookies to improve your experience on our site. By using our site, you consent to cookies.

Manage your cookie preferences below:

Essential cookies enable basic functions and are necessary for the proper function of the website.

These cookies are needed for adding comments on this website.

Google reCAPTCHA helps protect websites from spam and abuse by verifying user interactions through challenges.

Google Tag Manager simplifies the management of marketing tags on your website without code changes.

Statistics cookies collect information anonymously. This information helps us understand how visitors use our website.

Google Analytics is a powerful tool that tracks and analyzes website traffic for informed marketing decisions.

Service URL: policies.google.com (opens in a new window)

Marketing cookies are used to follow visitors to websites. The intention is to show ads that are relevant and engaging to the individual user.

Facebook Pixel is a web analytics service that tracks and reports website traffic.

Service URL: www.facebook.com (opens in a new window)