When it comes to senior care, the words “assisted living” and “skilled nursing” are often used as if they mean the same thing. They do not, and that distinction matters enormously when it comes to assisted living liability insurance and the broader world of long-term care facility insurance.

A facility owner or administrator who treats these two environments as interchangeable from an insurance standpoint is taking on a level of financial and legal risk that no business can afford.

Both types of facilities serve elderly or vulnerable populations. Both employ caregiving staff. Both face the possibility of lawsuits, accidents, and negligence claims. But the nature of care delivered, the level of medical intervention involved, and the regulatory environment governing each are fundamentally different. Those differences create entirely distinct liability insurance profiles, and understanding them is essential for protecting your facility, your staff, your residents, and your bottom line.

This guide breaks down the key insurance differences between assisted living facilities (ALFs) and skilled nursing facilities (SNFs), so you can make informed decisions about the coverage your operation truly needs.

What Is Assisted Living?

Assisted living is a long term housing option for older adults who do not need intensive medical care but still benefit from daily support. In an assisted living community in Concord, NH, staff members can help residents with personal care tasks such as bathing, dressing, eating, and other daily activities while encouraging them to remain as independent as possible.

These communities also support an active social lifestyle through planned events, group activities, outings, and opportunities to connect with other residents. Seniors can maintain their own routines and choose the activities that best fit their interests and comfort level.

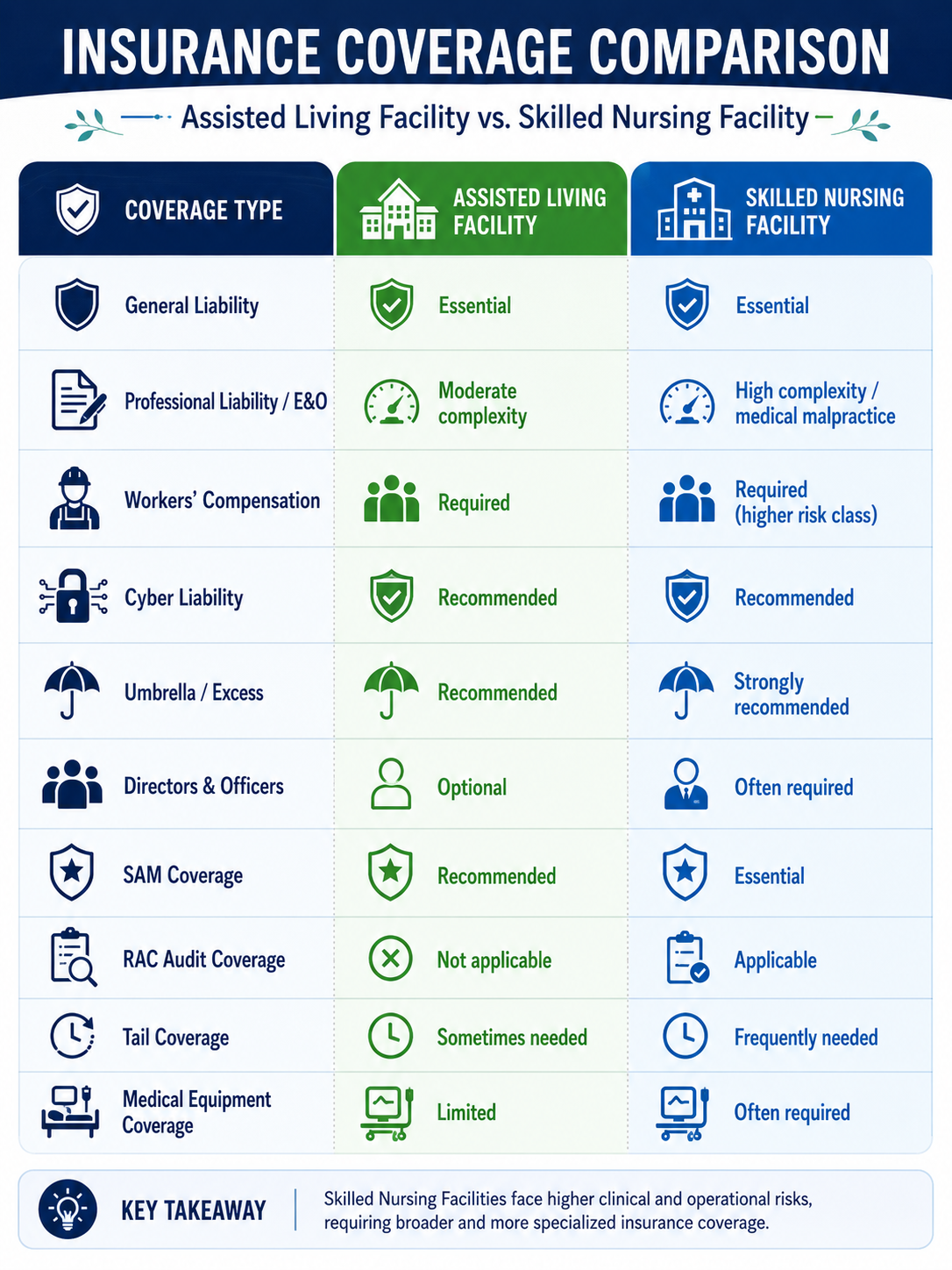

Assisted Living Liability Insurance: What Coverage Do You Need?

Selecting the right assisted living liability insurance means building a layered program that addresses the unique risk profile of a residential senior care environment. Here are the core coverage types every ALF operator should consider.

General Liability Insurance

General liability insurance protects assisted living facilities from third-party claims involving bodily injury, property damage, or personal injury on the premises. This may include incidents such as visitor slip-and-fall accidents, resident injuries in common areas, or property damage claims.

Professional Liability Insurance

Professional liability insurance, also known as E&O insurance, covers care-related claims in assisted living settings. It may apply when a staff member makes a medication error, fails to assist a resident properly, or is accused of negligent personal care.

Workers’ Compensation Insurance

Workers’ compensation insurance covers employees who are injured while performing job duties. In assisted living facilities, this is important because staff often help residents with transfers, mobility, lifting, and repositioning, which can lead to workplace injuries.

Cyber Liability Insurance

Cyber liability insurance helps protect assisted living facilities from the financial impact of data breaches and cyberattacks. This coverage is important because facilities store sensitive resident records, health information, financial details, and emergency contact data.

Umbrella / Excess Liability Insurance

Umbrella insurance provides extra protection when the limits of other policies are exhausted. It is especially useful for assisted living facilities because claims involving elderly or vulnerable residents can lead to costly lawsuits or large settlements.

How Much Does Assisted Living Cost?

Assisted living is usually more affordable than skilled nursing because residents typically need less intensive medical care. In Concord, New Hampshire, the monthly cost of a nursing home may be around $8,000, while assisted living is often a little over $5,500 per month.

This monthly fee commonly includes:

Rent

Utilities

Home maintenance

Trash removal

Landscaping

Housekeeping services

Dining

The total cost can vary based on the type of room or apartment selected. Larger living spaces usually cost more. For example, if a community offers both shared and private bathrooms, choosing a room with a private bathroom will typically increase the monthly cost.

What Is Skilled Nursing?

Skilled nursing facilities, also known as nursing homes, provide many of the same basic support services found in assisted living communities, along with 24 hour medical care. Many older adults move to skilled nursing after a major health event, such as a stroke, heart attack, surgery, or serious illness. They may no longer need hospital care, but they still require ongoing medical supervision to stay stable and recover safely.

Skilled nursing facilities also require a higher level of staffing than assisted living communities. In a certified skilled nursing facility, licensed practical nurses are available at all times, and a registered nurse is typically on duty for at least eight hours each day.

How Much Does Skilled Nursing Cost?

Because skilled nursing provides a higher level of medical care and daily support, it is usually one of the most expensive senior care options. In Concord, New Hampshire, the average cost of a nursing home is approximately $8,000 per month. This cost typically includes medical care, room, meals, utilities, and other daily living expenses.

The final monthly cost depends on the facility and the type of room selected. Private rooms usually cost more than semi-private rooms. In many cases, choosing a private room may add about $1,100 per month to the total cost.

Skilled Nursing Facility Liability Insurance: A More Complex Picture

Skilled nursing facility liability insurance encompasses all of the coverage types above, and considerably more. The heightened clinical complexity of SNF operations demands a more robust and specialized insurance program.

Medical Malpractice / Professional Liability Insurance

This is the core coverage for skilled nursing facilities because they provide direct clinical care, medication management, wound care, rehabilitation, IV therapy, and other medical services. It helps protect against claims involving medication errors, pressure ulcers, falls, sepsis, aspiration incidents, and other care-related risks.

General Liability Insurance

Skilled nursing facilities also need general liability insurance to cover third-party bodily injury and property damage. This is especially important because SNFs have more medical equipment, higher resident care needs, and frequent movement of staff, residents, and visitors throughout the facility.

Directors & Officers Insurance

D&O insurance protects owners, board members, executives, and administrators from claims related to leadership and management decisions. This may include lawsuits involving staffing levels, compliance policies, budget decisions, or changes in care procedures.

Sexual Abuse & Molestation Coverage

SAM coverage is essential for skilled nursing facilities because residents are often vulnerable and depend on staff for personal care. This coverage helps protect the facility against serious claims involving alleged staff misconduct, abuse, or neglect.

Workers’ Compensation Insurance

Workers’ compensation is legally required and important for SNFs because staff face high physical demands. Common risks include patient lifting, transfer injuries, exposure to illness, clinical procedure-related injuries, and incidents involving residents with behavioral challenges.

Recovery Audit Coverage and Tail Coverage

Recovery audit coverage helps skilled nursing facilities manage costs related to Medicare and Medicaid billing audits. Tail coverage is also important when switching or ending a policy because it helps protect against claims tied to incidents that happened during a previous coverage period.

Head-to-Head: Key Insurance Differences

Common Liability Risks Unique to Each Facility Type

Understanding assisted living vs skilled nursing risk exposure helps operators select the right level of long term care facility insurance for their specific environment.

Assisted Living Facility Claim Risks

- Falls in residential areas can lead to injury claims.

- Medication errors may happen when staff assist with resident medications.

- Resident elopement is a major risk in memory care units.

- Delayed escalation of worsening health conditions can create liability.

- These risks make general and professional liability coverage important.

Skilled Nursing Facility Claim Risks

- Pressure ulcer neglect can lead to serious claims.

- Poor wound care may result in infection or sepsis.

- High-risk medication errors can cause severe harm.

- Poor post-surgical supervision can lead to complications.

- Improper restraint use can create legal and regulatory risk.

- Inadequate staffing can result in preventable resident decline.

- These risks make comprehensive nursing home liability coverage essential.

How to Choose the Right Senior Care Facility Insurance Partner

Not all commercial insurers understand the senior care space. For both ALFs and SNFs, working with a specialty broker who has deep experience in long term care facility insurance and senior living is essential. When evaluating partners for your assisted living liability insurance or skilled nursing facility liability insurance needs, look for a partner who:

- Understands the regulatory landscape in your state (for ALFs) or under CMS (for SNFs)

- Can build a layered insurance program that eliminates gaps between policies

- Offers risk management support, not just policy placement

- Has access to a wide range of carriers specializing in senior care facility insurance

- Can advise on alternative risk financing options, such as captive insurance structures, for larger operators

- Has a demonstrated track record placing professional liability insurance for nursing homes and ALFs

Conclusion

When it comes to assisted living vs skilled nursing, both facility types serve some of society’s most vulnerable members, and both carry significant legal and financial risk as a result. But the nature of that risk, and the long term care facility insurance required to address it, is meaningfully different between the two.

For assisted living operators, the priority is building a solid foundation of assisted living liability insurance, general liability, professional liability, and workers’ compensation, layered with cyber and umbrella protection. For skilled nursing facilities, the program must go further: addressing medical malpractice exposure through professional liability insurance for nursing homes, executive liability through D&O, and the specialized risks that come with CMS participation under a comprehensive skilled nursing facility liability insurance framework.