Professionals with claims-made malpractice insurance may qualify for free tail coverage when they permanently retire from practice. Most insurers require continuous coverage with the same carrier, a minimum retirement age, and a clean claims history. Meeting these requirements can help retiring professionals avoid paying a large one-time premium for extended reporting protection.

Why Tail Coverage Matters When Planning Retirement?

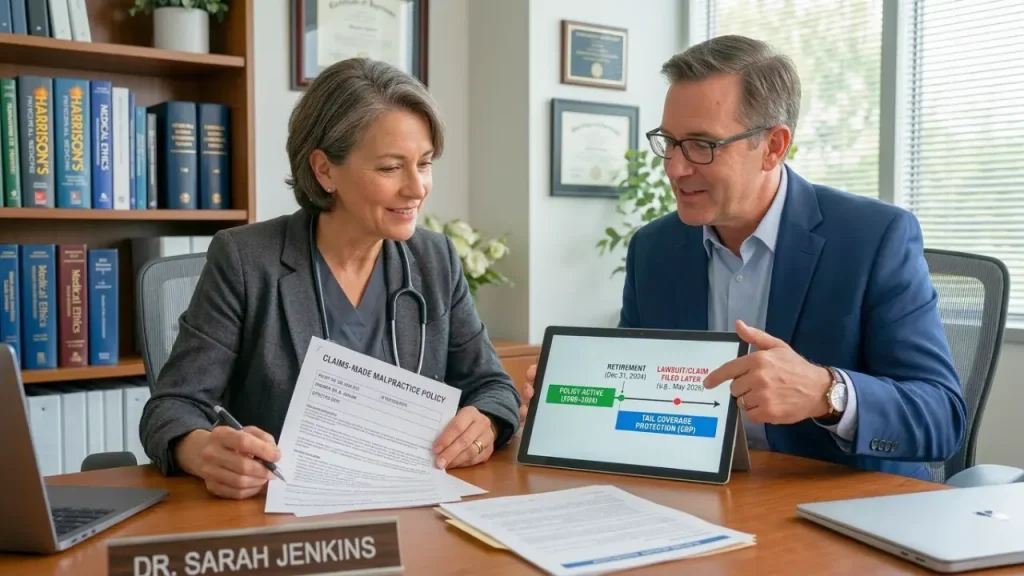

Planning retirement involves more than financial investments and lifestyle decisions. For physicians and healthcare providers, securing the right medical malpractice insurance, especially tail coverage to protect against claims filed after retirement, is a critical part of a well-structured exit strategy. Without proper coverage in place, even past clinical decisions can create financial and legal risks long after leaving practice. Incorporating insurance into retirement planning helps ensure long-term peace of mind and financial security.

Many professionals assume their malpractice insurance automatically protects them even after they stop practicing. However, most policies are written as claims-made policies, meaning coverage only applies if the claim is reported while the policy is active.

This is where tail coverage insurance becomes important.

Tail coverage allows professionals to report claims after their policy ends, as long as the incident occurred while the policy was active. Without this protection, a claim filed years after retirement could leave a professional responsible for legal defense costs and potential settlements.

The good news is that many insurers offer free tail coverage for professionals who meet certain retirement requirements. Understanding how to qualify for free tail coverage early in your career or retirement planning can potentially save thousands of dollars.

For professionals reviewing their coverage, consulting with an experienced advisor such as PLI Consultant can help clarify eligibility rules and ensure the right protection is in place before retirement.

What Is Tail Coverage in Malpractice Insurance?

Tail coverage malpractice protection, also known as extended reporting period (ERP) coverage, allows professionals to report claims after their claims-made policy has ended.

In simple terms, malpractice insurance tail coverage extends the time allowed to report claims related to past professional services.

Tail coverage protects professionals by:

- Allowing claims to be reported after a policy ends

- Covering services performed while the policy was active

Protecting against delayed malpractice claims - Maintaining protection during retirement or career transitions

Because many malpractice claims are filed years after the original work was performed, tail end insurance coverage is essential for professionals who are retiring or leaving a practice.

Why Retiring Professionals Need Tail Coverage

Even after retirement, professionals can still face legal claims related to services performed earlier in their careers.

Consider this scenario:

- An attorney completes legal work for a client in 2024

- The attorney retires in 2027

- The client files a malpractice claim in 2029

If the attorney had a claims-made policy that ended upon retirement and did not purchase malpractice insurance tail coverage, the claim would not be covered.

This is why tail coverage for retiring professionals is so important. It ensures protection against claims that arise after retirement but relate to past work.

Without tail coverage, professionals may face:

- Significant legal defense costs

- Personal financial liability

- Damage to professional reputation

Proper retirement planning should always include reviewing tail coverage malpractice protection options.

What Is Free Tail Coverage?

Free tail coverage is a retirement benefit offered by some malpractice insurers. It allows eligible professionals to obtain extended reporting protection without paying the typical one-time premium.

This benefit is commonly called retirement tail coverage.

Instead of purchasing coverage separately, qualifying professionals receive tail coverage automatically when they permanently retire and meet the insurer’s eligibility requirements.

For many professionals, this can represent substantial savings because tail coverage insurance can be expensive when purchased independently.

This is why understanding how to qualify for free tail coverage is such an important part of retirement planning and we’ll explore this in detail later in the blog.

Professionals unsure about eligibility or policy details can consult insurance specialists like PLI Consultant to evaluate their coverage and confirm retirement options.

How Much Is Tail Coverage?

One of the most common questions professionals ask is how much tail coverage is when it is not included for free.

In most cases, tail coverage insurance costs between 150% to 300% of the final annual malpractice premium. This amount is usually paid as a one-time premium when the policy ends.

Example Tail Coverage Costs

Annual Malpractice Premium | Estimated Tail Coverage Cost |

$3,000 | $6,000 – $9,000 |

$5,000 | $10,000 – $15,000 |

$8,000 | $16,000 – $24,000 |

Once purchased, tail-end insurance coverage typically remains in effect indefinitely for claims related to past work.

Factors That Affect Tail Coverage Pricing

Several factors influence malpractice insurance tail coverage costs:

- Professional specialty or practice area

- State malpractice risk levels

- Claims history

- Policy limits and coverage structure

- Insurance carrier underwriting guidelines

Because the cost can be significant, qualifying for free tail coverage can provide major financial relief when planning retirement.

How to Qualify for Free Tail Coverage?

Understanding how to qualify for free tail coverage requires reviewing the eligibility criteria established by the insurance carrier. While requirements vary, most insurers follow similar guidelines.

Professionals may qualify for free retirement tail coverage if they:

- Permanently retire from professional practice

- Meet a minimum retirement age (often 55 or older)

- Maintain continuous coverage with the same insurer for several years

- Have a stable claims history

- Keep their malpractice policy active until retirement

These requirements help insurers ensure that the professional maintains responsible coverage throughout their career.

Before retiring, professionals should confirm their eligibility directly with their insurance provider or consult a specialist, such as a PLI Consultant, to review their policy.

Key Factors That Determine Eligibility

Several factors can influence whether a professional qualifies for free tail coverage.

Permanent Retirement

Most insurers require professionals to retire from their practice fully. Continuing to provide services, even part-time, may disqualify eligibility for retirement tail coverage.

Length of Time With the Same Insurance Carrier

Insurance companies often require professionals to maintain coverage with the same carrier for three to five consecutive years before retirement.

This requirement helps insurers evaluate risk and establish a long-term relationship with policyholders.

Claims History

Professionals with minimal or no malpractice claims are more likely to qualify for malpractice tail coverage retirement benefits.

A clean claims record indicates lower long-term risk for the insurer.

Age Requirements

Some insurers set a minimum retirement age for eligibility. This is commonly age 55 or 60, although the exact requirement depends on the insurance carrier.

Continuous Coverage

Professionals must maintain active tail coverage insurance eligibility by ensuring their malpractice policy remains in force until the official retirement date.

Retirement Planning Timeline for Tail Coverage

Planning is essential for professionals who want to qualify for retirement tail coverage.

- Five Years Before Retirement: Professionals should review their malpractice insurance structure and confirm whether their policy is claims-made or occurrence-based.

- Two to Three Years Before Retirement: Contact the insurance provider to discuss tail coverage, malpractice protection, and verify eligibility for free retirement coverage.

- One Year Before Retirement: Confirm retirement plans, verify policy requirements, and ensure there are no coverage gaps. Consulting with professionals, such as a PLI Consultant, during this stage can help ensure the retirement transition is handled correctly.

Common Mistakes That Prevent Free Tail Coverage

Some professionals unintentionally lose eligibility for free tail coverage because of avoidable mistakes.

Common issues include:

- Switching insurance carriers shortly before retirement

- Allowing malpractice insurance to lapse

- Continuing part-time consulting work after retirement

- Failing to review eligibility requirements in advance

These mistakes may require professionals to purchase tail coverage insurance at full price. Planning can help avoid these costly outcomes.

What If You Don’t Qualify for Free Tail Coverage?

Not every professional qualifies for free retirement tail coverage, but there are still several options available.

Purchase Tail Coverage

Professionals can purchase malpractice insurance tail coverage directly from their current insurer.

Although the cost can be high, it provides essential protection for claims related to past work.

Employer-Sponsored Coverage

Some firms or organizations provide tail coverage for retiring professionals as part of a retirement agreement or employment contract.

Prior Acts Coverage

In some cases, a new insurer may offer prior acts coverage, which protects services performed before the new policy began.

Professionals should review these options carefully before retiring.

How to Check Your Tail Coverage Eligibility?

Professionals approaching retirement should take several steps to confirm their eligibility for free tail coverage.

Recommended steps include:

- Review your malpractice policy type

- Confirm whether it is a claims-made policy

- Contact your insurance provider

- Ask about eligibility for retirement tail coverage

- Verify requirements in writing

Working with insurance advisors such as PLI Consultant can help ensure the policy structure aligns with retirement goals.

Get Professional Guidance Before You Retire

Every professional’s malpractice policy is different. The terms, eligibility rules, and coverage limits can vary between insurance providers.

Before retiring, it is important to confirm whether you qualify for free tail coverage and understand the cost of tail coverage malpractice protection if you do not.

Experienced advisors like PLI Consultant can help professionals:

- Review malpractice insurance policies

- Confirm eligibility for retirement tail coverage

- Compare coverage options

- Avoid unexpected insurance costs during retirement

Taking these steps early ensures a smoother transition into retirement and continued protection against future claims.