As a healthcare professional, it is important to understand exactly what your malpractice insurance, also known as medical professional liability insurance, does and does not cover.

This coverage can protect you from certain legal and financial risks related to patient care, but it is not unlimited. Knowing the policy’s scope, exclusions, and coverage limits helps you avoid unexpected gaps and make sure your professional protection is strong enough for your practice.

PLI Consultants helps healthcare professionals compare malpractice insurance options, understand carrier differences, and review coverage details before small policy gaps turn into expensive problems.

What Is Medical Malpractice Insurance?

Medical malpractice insurance, also known as medical liability insurance, protects healthcare providers against claims related to errors, negligence, or alleged mistakes that occur while delivering medical care.

These policies typically cover legal defense costs and claims involving medical errors or negligence, even when the allegations are false or without merit. However, coverage does not usually apply to intentional misconduct or criminal acts. In some cases, a policy may cover defense costs until it is determined whether the act falls outside the scope of coverage.

For more details: See our guide to medical malpractice insurance coverage

What Does Medical Malpractice Insurance Usually Cover?

A standard medical malpractice policy may cover several major claim-related expenses, depending on the policy language.

What Does Medical Malpractice Insurance Usually Exclude?

Medical malpractice insurance is not an all-purpose business protection policy. It is designed for covered professional liability claims. Most policies contain exclusions that limit or remove coverage for certain acts, services, or situations.

Intentional or Criminal Acts

Malpractice insurance is designed to cover negligence, not deliberate harm or criminal conduct. If a provider intentionally injures a patient, commits fraud, or engages in criminal behavior, the policy may deny coverage.

This is one of the clearest exclusions in most professional liability policies.

Sexual Misconduct

Claims involving sexual misconduct are commonly excluded from malpractice coverage. Even if a claim arises in a healthcare setting, insurers often treat this type of allegation separately from professional negligence.

Some policies may provide a limited defense until facts are established, but providers should never assume full coverage applies.

Known Prior Claims or Incidents

A provider usually cannot buy a new policy to cover a claim or incident they already knew about and failed to disclose. Applications often ask about prior claims, potential claims, board actions, or known incidents.

If a provider gives incomplete or inaccurate information, the insurer may deny coverage or cancel the policy.

Services Outside the Policy Scope

A malpractice policy is written around specific professional services. If a physician starts offering services not listed in the policy, such as cosmetic procedures, telemedicine across state lines, weight loss treatments, medical spa services, or new surgical procedures, those services may not be covered unless the policy is updated.

This is a major issue for growing practices. Coverage should be reviewed whenever services, locations, staffing, or patient volume changes.

Alteration of Medical Records

Improperly changing, deleting, or falsifying medical records can create serious coverage problems. Medical records are central to malpractice defense. If a provider alters records after an incident, the insurer may treat the action as intentional misconduct or a policy violation.

Accurate documentation is not just a clinical issue. It is also a coverage issue.

Cyber Liability and Data Breaches

Medical malpractice insurance does not always cover cyber events, HIPAA-related privacy incidents, ransomware attacks, or patient data breaches. Some policies include limited cyber protection, but many providers need a separate cyber liability policy.

For practices that use electronic health records, online scheduling, billing platforms, telemedicine tools, or patient portals, cyber coverage should be reviewed separately.

General Business Risks

Malpractice insurance usually does not replace general liability, property insurance, workers’ compensation, employment practices liability, or business owner coverage.

For example, malpractice insurance may not cover a slip and fall in the waiting room, employee discrimination claims, property damage, payroll disputes, or office equipment losses. These risks usually require separate policies.

Contractual Liability Beyond the Policy

Some employment contracts, hospital agreements, or vendor contracts may include indemnification language. A malpractice policy may not cover every liability a provider agrees to assume by contract.

Before signing a contract, providers should check whether the insurance policy supports the contract requirements. This is especially important for independent contractors, locum tenens physicians, telemedicine providers, and private practice owners.

Key Policy Terms Providers Should Review

The covered versus excluded question cannot be answered from the premium alone. A cheaper policy may have weaker terms, lower limits, narrower coverage, or more restrictive exclusions.

How to Avoid Malpractice Coverage Gaps?

The best time to review your malpractice insurance is before a claim, before a job change, and before signing a contract. Do not wait until you receive a lawsuit, board notice, or patient demand letter. A proactive review should include:

- Request the full policy document, not just the certificate of insurance

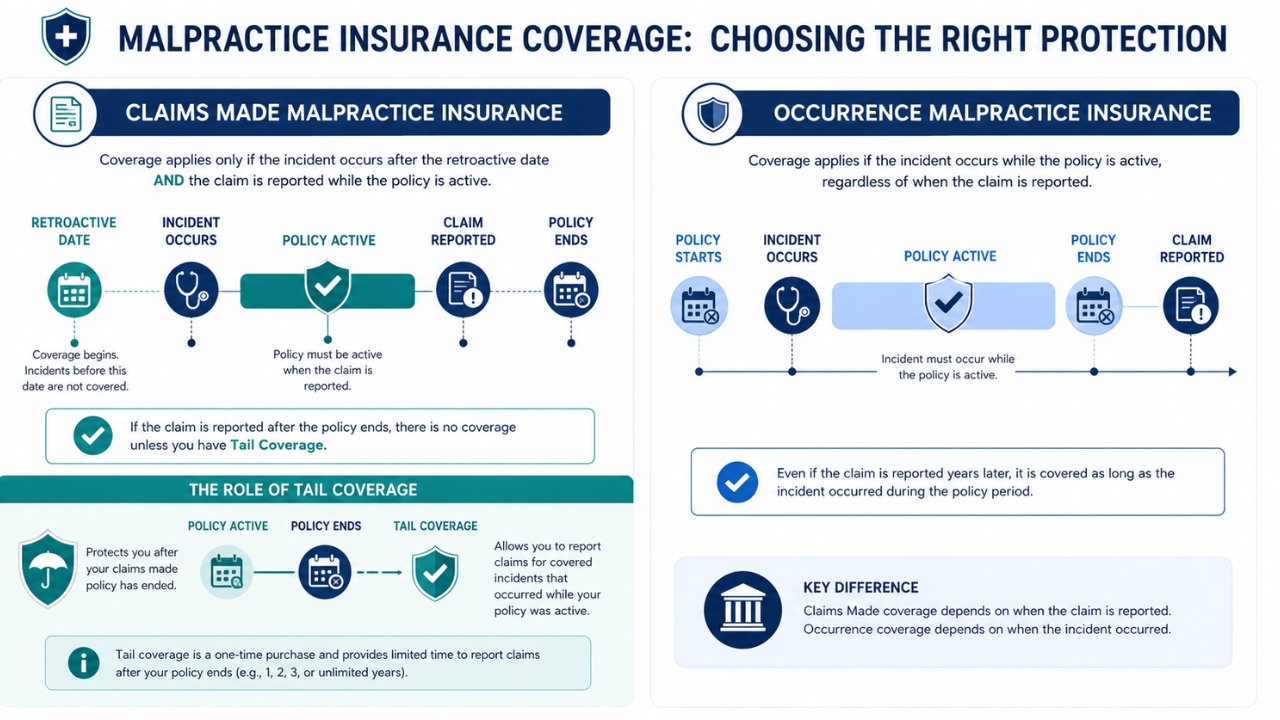

- Confirm whether the policy is claims-made or occurrence

- Check the retroactive date on claims-made coverage

- Clarify who pays for tail coverage when employment ends

- Confirm whether prior acts coverage is available with a new carrier

- Review exclusions specific to your specialty and procedures

- Verify whether defense costs reduce your liability limits

- Ensure all locations, entities, and services are listed and covered

- Keep copies of declarations pages and any cancellation notices

- Review coverage whenever your role, practice model, or employer changes

PLI Consultants works with healthcare professionals who want a clearer picture of what their malpractice policy does — and does not — protect against.

Final Takeaway

Medical malpractice insurance can protect healthcare providers from the financial impact of covered negligence claims, but it does not cover everything. The real protection depends on policy type, limits, exclusions, reporting rules, defense cost language, and tail coverage terms.

For physicians and healthcare practices, the safest approach is to review the full policy before choosing coverage, changing employers, adding services, or signing contracts. A well-matched malpractice policy does more than meet a requirement. It helps protect your career, assets, and future practice stability.